Independent central banks are important institutions that contribute to economic stability and prosperity. Empirically, countries with independent central banks have lower inflation, yet similar or greater GDP growth and employment. By contrast, when central banks are easily pressured by the executive or legislative branches, episodes of high inflation become more likely. Less-independent central banks also can become piggybanks for funding inefficient industries.

Yet our democratic order does not countenance a completely independent institution that can create or lend money as it wishes. And our administrative state is full of semi-independent institutions whose missions have crept and drifted. Independence must always be constrained by limited authority and ultimate responsibility to elected officials, and through them to the people. The Federal Reserve has no independent rights or independence. It is created by Congress, to serve the long-run interests of the American people.

In the United States, our founding principles of a separation of powers, checks and balances, and democratic accountability run counter to the concept of a central bank isolated from political pressure. “Political pressure” when the other party is in power is praised as “democratic accountability” when your party is in power. Americans have also long feared concentrated bank power.

Power struggles

US history is punctuated by a tussle between fear of concentrated power and financial instability. In 1790, Treasury Secretary Alexander Hamilton proposed that the federal government should establish a national bank. The bank, like the Bank of England, could issue banknotes to serve as a uniform currency, make loans to the government and businesses, and act as the government’s fiscal agent making a market in government debt, and provide stability to the banking system. (Under the gold standard, early central banks were not responsible for inflation, but focused on these important financial and banking roles.) Thomas Jefferson objected that no such power was enumerated in the Constitution and that such an institution would concentrate too much power. Hamilton’s appeal to implied powers persuaded President Washington, and the First Bank of the United States was established. Though its charter was allowed to expire after twenty years, Hamilton’s arguments later became legal precedent as the Doctrine of Implied Powers, which broadly expanded federal authority.

Despite persistent popular aversion to concentrated bank power, the Second Bank of the United States was founded in 1816, largely in response to the financial crises stemming from the War of 1812. Sixteen years later, after a bitter fight with bank president Nicholas Biddle, President Andrew Jackson vetoed its recharter.

Repeated financial crises through the 19th and early 20th centuries renewed interest in a national bank. The Federal Reserve was founded largely in response to the panic of 1907 and the desire for a formal lender of last resort. The debate around the Federal Reserve’s creation in 1913 turned less on constitutional questions than on fears about concentrated bank power in financial centers like New York. The resulting Federal Reserve System mixed a fully public Board of Governors with twelve regional quasi-private federal reserve banks. The regional banks perform an important function in representing regional interests, gathering regional information, and thereby gaining widespread support for Federal Reserve activities.

During its first twenty years, the Fed operated with minimal oversight, though two presidential appointees—the treasury secretary and the comptroller of the currency—sat on its board.

The Fed became more independent in the 1930s in two ways. The Banking Act of 1935 removed the treasury secretary and the comptroller of the currency from the Board of Governors, and the Humphrey’s Executor decision upheld the constitutionality of independent agencies whose members the president could not remove at will.

Independence eroded in and after World War II. In April 1942, the Treasury asked the Fed to hold interest rates near zero to help finance the war. The Fed did not object, voluntarily accepting some inflationary danger given the exigency of war. After the war, however, the Treasury insisted that the Fed buy Treasury bonds as needed with newly created money to maintain a 2.25 percent cap on long-term bond yields. Prices rose nearly 30 percent in just three years. After an acrimonious battle, the Fed re-established its independent authority over bond purchases with the Treasury-Fed Accord of March 1951.

Independence eroded again under Presidents Johnson and Nixon. The latter in particular pressured Fed Chair Arthur Burns to stimulate the economy before the 1972 election. Stimulative fiscal and monetary policy, combined with price controls, the OPEC oil shocks, and the breakdown of the Bretton Woods system created stagflation.

Congress responded with new Fed accountability requirements—including semiannual reports and congressional testimony by the Fed chair—and the Federal Reserve Reform Act of 1977, which directed the Fed to “promote the goals of maximum employment, stable prices, and moderate long-term interest rates.” Independence lives within a specific mandate and accountability to elected officials. Chastened by the economic and political consequences of Nixon’s interference, both Presidents Carter and Reagan supported Chair Paul Volcker’s large interest rate hikes to fight inflation, despite their short-run recessionary effects.

Still, the poor performance of the 1970s is also a story of Federal Reserve policy mistakes, not of untoward political pressure. Independence alone does not guarantee good policy.

Virtues of independence

The case for central bank independence was greatly strengthened by an academic literature that started in the late 1970s. Macroeconomic models, summarizing wide experience, showed that output and employment can only be raised by a surprise inflation, greater than what people expect. Governments face a continual temptation to surprise the public with inflation to get the short-run output boost. But governments can’t surprise people every day. They soon catch on, and the government reaps only inflation, not any higher employment.

Governments need to find a way to precommit, to tie their hands to the mast not to inflate next year, in order to produce low inflation and high employment today.

That only happens if they are unable to inflate tomorrow. Independent central banks are part of that commitment mechanism: The government can appoint inflation-averse “hawks” as central bankers and insulate them from political and public pressure.

The limited authority of central banks is another important precommitment against inflation. The US Fed may not buy bonds directly from the Treasury, and must always buy and sell rather than print money and hand it out. Other central banks have been forbidden to buy treasury debt at all, to prevent them from monetizing deficits.

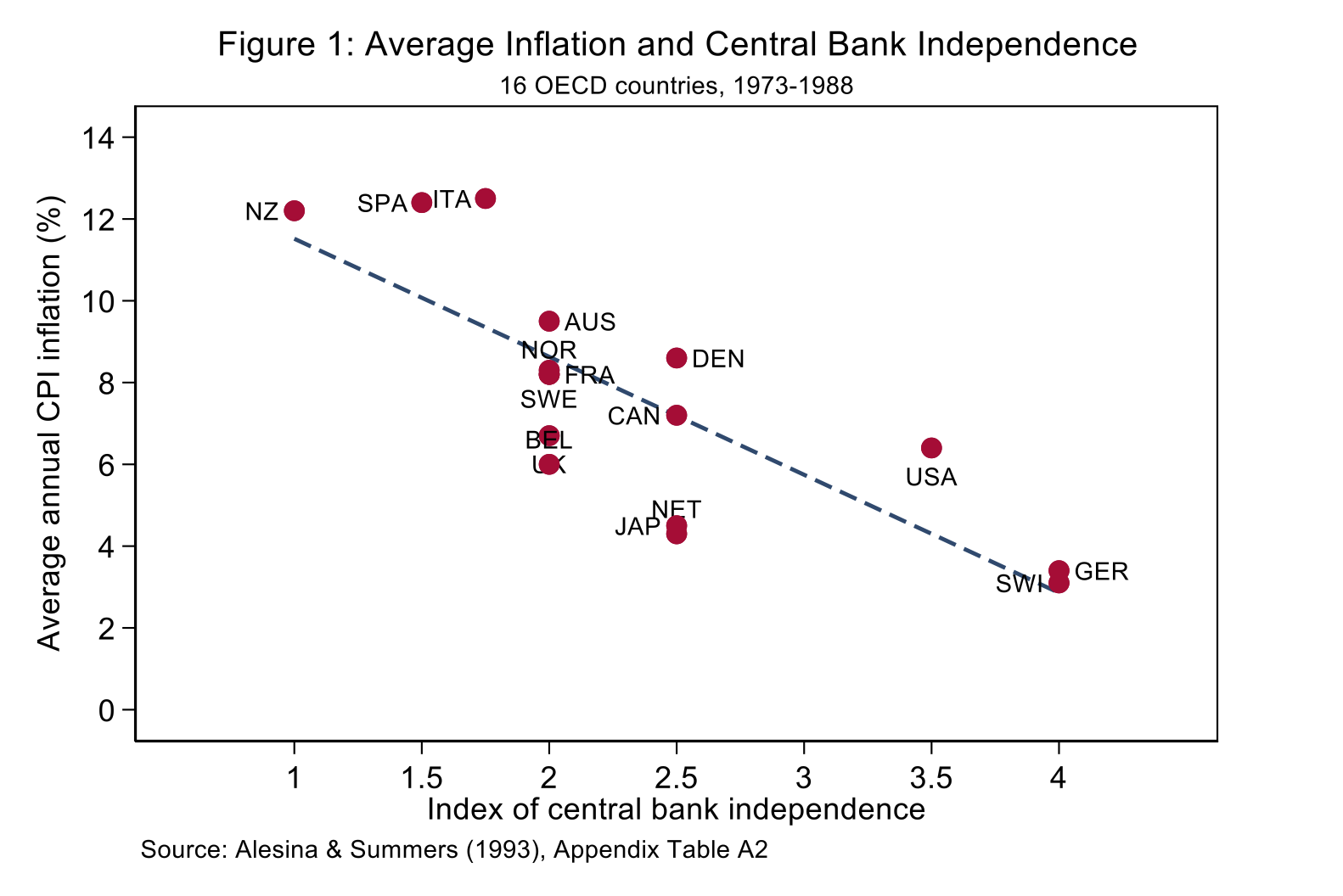

An empirical literature tested these theories. The results were striking. Figure 1 reproduces a classic finding from Alberto Alesina and Larry Summers (1993), plotting average annual inflation from 1973 to 1988 against an index of central bank independence for sixteen OECD countries. The negative relationship is strong and statistically significant: more-independent central banks deliver lower average inflation.

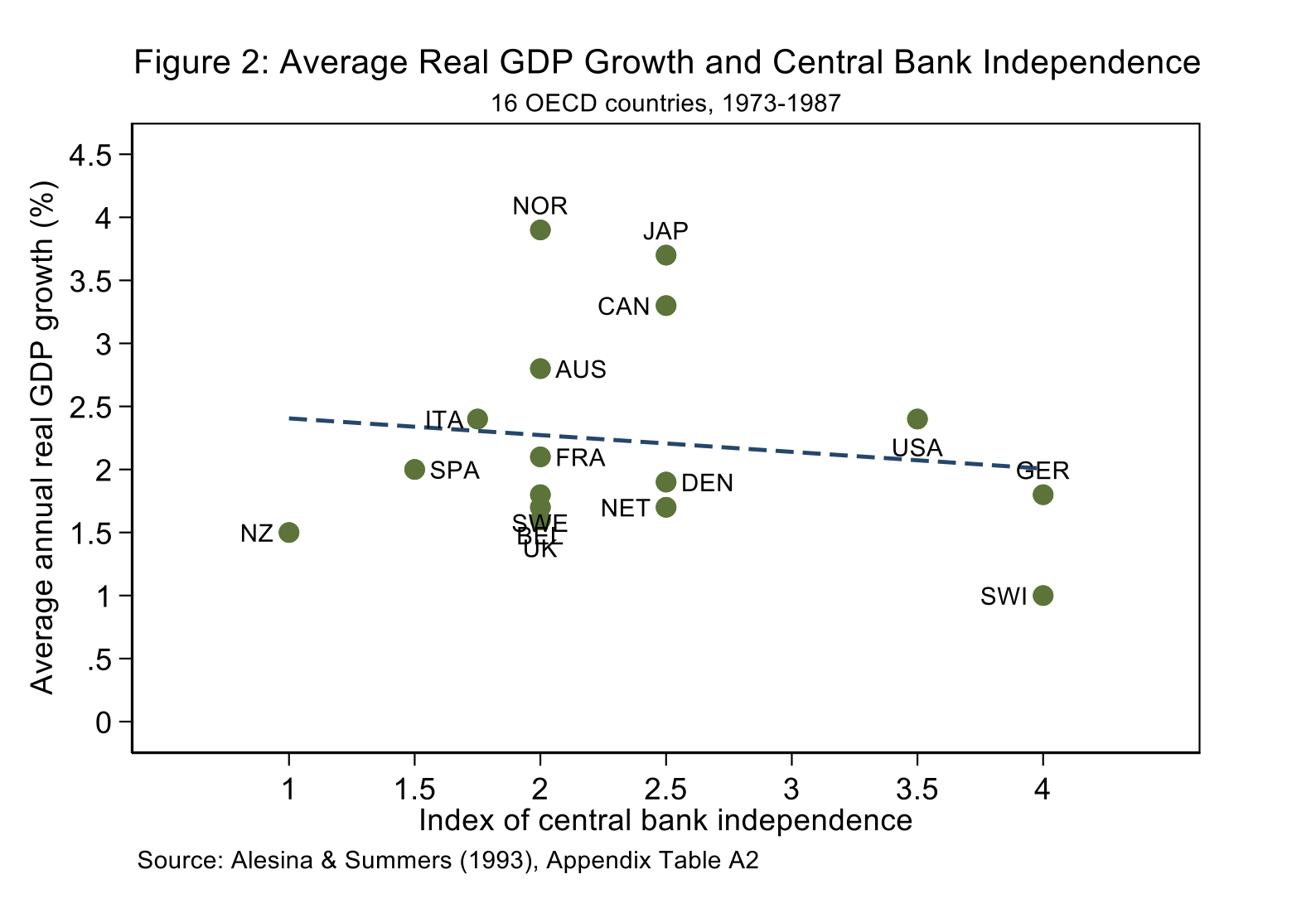

One might worry that a central bank narrowly focused on inflation would sacrifice growth. Figure 2 rejects that concern: the relationship between independence and average GDP growth is small and not statistically significant. Follow-up work using different measures of independence and broader country samples reaches similar conclusions. Politically dependent central banks are particularly prone to inflation and credit allocation in less developed countries, with more deleterious effects on economic growth.

These academic findings shaped the foundation of a major international institution: the European Central Bank. The 1992 Maastricht Treaty made the ECB independent of member-state political influence, isolated from fiscal pressures, and gave it a primary mandate of price stability. Whatever the ECB’s troubles with sovereign bailouts and inflation, those do not come from inadequate independence.

Rising pressure

In the United States, an independent Fed is particularly important at this juncture in history. But the challenge is much greater than a simple repetition of a president’s desire for low interest rates, as in the 1970s. We are facing a situation more like that before the 1951 Accord.

With federal government debt at 100 percent of GDP, politicians showing no inclination to reduce deficits, and a habit of meeting every crisis with a river of money, fiscal pressures will challenge monetary policy.

It is always tempting to inflate away debt. The COVID and post-COVID deficits were largely paid for by inflating away approximately 15 percent of the value of debt. Moreover, every percentage point that the Fed raises interest rates is another percentage point of interest cost on the federal debt, adding a percentage point of GDP extra deficit, which will not be welcomed by Congress and the administration. The Fed already faces pressure to hold down interest costs.

The Fed cooperated voluntarily with the inflationary policies of 2020–21 by holding interest rates at zero, buying the majority of the new debt issues, and widespread financial support. Avoiding a repetition of that inflation requires a Fed that has the mandate and authority not to cooperate with fiscal inflationary forces, and the independence to stand up to what will surely be strong pressure. Otherwise, the United States will see another “Great Inflation.”

Long before President Trump came along, the Fed had dramatically increased the scope of its activities. The Fed can remain independent only if it works within a narrow mandate. If the Fed steps too far into fiscal policy, directing credit, telling banks what to do, or other politically sensitive areas, it must become more politically accountable and less independent. Economic theory and historical experience show that when monetary policy is asked to deliver multiple “primary” goals, it tends to fail on the most important ones: price stability and financial stability.

A new Fed-Treasury accord separating monetary and fiscal policy, a renewed and narrowed congressional mandate, and internal efforts to reduce the Fed’s footprint as our colleague Kevin Warsh has proposed, are all important ancillaries for the Fed to regain and enhance its important independence, within our order of accountable government limited by checks and balances.

John H. Cochrane is the Rose-Marie and Jack Anderson Senior Fellow at the Hoover Institution. He is also a senior fellow of the Stanford Institute for Economic Policy Research (SIEPR), professor of finance and economics (by courtesy) at Stanford University’s Graduate School of Business, a research associate of the National Bureau of Economic Research, and an adjunct scholar of the Cato Institute. He also authors a popular Substack called The Grumpy Economist.

Valerie A. Ramey is the Thomas Sowell Senior Fellow at the Hoover Institution. She is also a research associate of the National Bureau of Economic Research, a research fellow of the Centre for Economic Policy Research, a member of the American Academy of Arts and Sciences, and a fellow of the Econometric Society.