Trump administration apologists portray its trade policies as an overdue correction to an international trade system that has been fundamentally unfair to the United States for decades. In the words of former US trade representative Robert Lighthizer, President Trump’s agenda is the “necessary first step” toward a transformed system “built on the principles of balance, transparency, and sovereignty.”

This article is part of The Commons Dispatch, a channel produced in partnership with the Hoover Institution’s Economic and Security Commons initiative, which draws on America’s constitutional principles and reflects the Hoover Institution’s founding commitments: to advance freedom and to address the world’s shared challenges.

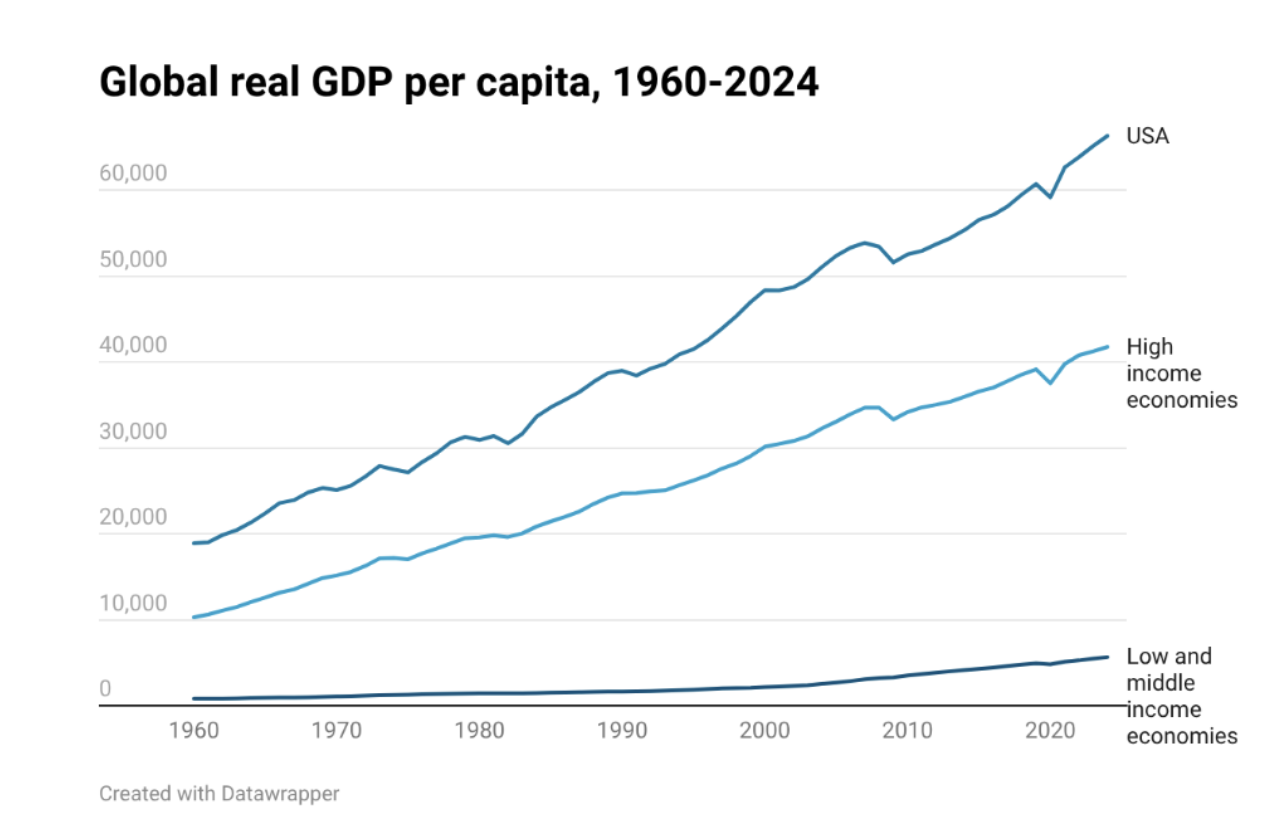

The claim that the trade system needs Trump’s harsh medicine because it has disproportionately rewarded foreign countries while harming the United States has no factual basis. The figure below shows the progress of global real GDP per capita since 1960. True, poorer countries have advanced relatively quickly from very low income levels, as one would wish in pursuit of a peaceful and prosperous world. But these countries, as well as other advanced economies, remain far behind the United States.

The grievance narrative that motivates Trump and supporters like Lighthizer is a mirage. True, some Americans have lost ground in the past three decades, but failures of domestic policy rather than trade policy deserve most of the blame.

And although the three trade system principles that Lighthizer advocates—balance, transparency, and sovereignty—are laudable, the reality of US economic statecraft since January 2025 distorts every one of them. Trump is indeed transforming the global economic system, but in a nationalistic direction that will serve neither America nor its trading partners in the long run.

In search of balance

With a mercurial deployment of tariffs in pursuit of a shifting range of economic and political demands, Trump’s trade policies are anything but transparent. Nor does his predatory behavior toward trade partners indicate much motivating respect for the sovereignty of other nations.

It may be more defensible to claim that the president is pursuing a rebalancing in international economic relations. Is there a sense in which Trump’s approach reshapes the international trade system toward a more desirable state of economic balance?

Who can object to “balance,” or advocate “imbalance”? Without a broadly agreed definition of the words, there is no way even to debate whether less imbalance would be helpful, whom it would help, or if the cure might be worse than the disease.

The Trump administration has appealed to a variety of concepts of balance in international trade. Sometimes it is the trade balance in goods, sometimes it is the trade balance in goods and services, sometimes it is the current account balance (which adds to the trade balance the balances on international investment income and international transfers), sometimes it is the US net international investment position (or NIIP, the balance of US foreign assets and liabilities).

Another policy-relevant distinction is between aggregate or overall US balances and bilateral balances with particular trade partners. In justifying his “Liberation Day” tariffs of April 2, 2025, Trump blamed persistent US trade imbalances on “lack of reciprocity in our bilateral trading relationships” and to repair these, he proposed country-specific tariffs intended to eliminate all of America’s bilateral trade deficits. Countries running trade deficits with the United States were not spared from tariffs: even in those cases, the Trump administration moved to curtail trade while extracting revenue from US businesses and consumers. Many of these so-called “reciprocal tariff” plans were modified later in response to US demands for trade access concessions, import commitments, or other considerations, including large pledges of investment funds to be placed under presidential control, without evident transparency or accountability.

The demand that US trade be balanced country by country, however, perverts the main purpose of international trade, which is that countries specialize in products they have a relative efficiency advantage in making, while importing the other goods they need from countries that can make them more cheaply. In practice, this principle will leave trade unbalanced across industries and even across trade partners. Botswana, for instance, typically has a bilateral trade surplus with the United States, which imports high-value diamonds while Botswana sources most of its own imports from lower-cost and less distant suppliers such as South Africa and Namibia. Only rarely does Botswana import commercial aircraft, where the United States has a comparative advantage, and when it does, it buys smaller, cheaper planes from producers such as Brazil’s Embraer to serve its limited domestic market.

More sophisticated economic nationalists (Lighthizer included) recognize the futility of insisting on country-by-country balanced trade but still idealize overall balance between imports and exports. Put bluntly, this prescription makes no economic sense as a general rule.

A standard critique of current account deficits is that they represent a transfer of wealth to foreigners, impoverishing the nation. As Lighthizer puts it, “A consistent deficit . . . [makes] a country poorer by transferring ownership of its assets overseas in exchange for current consumption.” The key omission is that countries run deficits not only to consume but also to invest beyond their available current income, and for the United States, those investments have yielded a return in excess of their cost, raising US national wealth. For the United States as well as most other countries, defining “balance” as a rejection of any net foreign financing is a recipe for impoverishment, not growth.

A large negative NIIP, such as that of the United States has currently (−$27.5 trillion at the end of last year), reflects in part past current account deficits but also factors that clearly flow from economic success. For example, the US NIIP (excluding derivatives, a minor component) fell by a whopping $6.2 trillion (21 percent of that year’s GDP) in 2024, to the alarm of believers in the damaging effects of foreign deficits. But of that fall, only $1.1 trillion was due to the current account deficit. An additional $3.8 trillion came from the outperformance of the US stock market in that year, which benefited foreign holders of US equities who had provided funds for American companies to invest, but benefited US residents even more. And a further $1 trillion came from the US dollar’s appreciation that year (the US is a net dollar borrower), which improved Americans’ terms of international trade.

Is a large negative NIIP a source of vulnerability to financial crisis? Individual borrowers, not the United States as a nation, hold the assets and liabilities that net out to the NIIP; those individuals, and not necessarily the nation, therefore face any related financial risks. It is only when a US borrower is large enough to destabilize the financial system as a whole (for example, a major interconnected bank) that its exposures can become a national threat. By far the biggest and most systemic US borrower is the federal government, with about 30 percent of its enormous debt held by overseas lenders who care about the risk of dollar depreciation against their home currencies. A potential US government debt crisis, as JPMorgan Chase CEO Jamie Dimon has warned, would destabilize the US as well as global economies.

A lower federal budget deficit attenuates the strongest single link between the negative US NIIP and crisis risk, while reducing the US current account deficit as well. Sadly, the Trump administration’s policies are only making that goal more distant, even though the US national debt is the biggest single threat connected with America’s current account deficit.

Trade deficit catastophizers also claim that deficits reduce GDP directly and squeeze manufacturing employment. The first claim rests on a failure to understand that trade deficits are most likely to expand when domestic spending, and hence output, is high. The second ignores that as incomes rise over time, manufacturing employment has eventually started to decline in all economies, even China’s, regardless of whether the country has an external deficit or surplus. The main driver, as Robert Lawrence explains in his masterful survey, is rising manufacturing productivity, which both allows more goods to be manufactured with less labor and generates an ever-higher demand for services.

To be sure, structural changes, whether from technological developments or trade, can disrupt industries and can cause concentrated unemployment that harms communities as well as individuals. Such changes are behind millions of job losses each year, as well as job creation in sectors that are favored. Most such changes have nothing to do with trade. Addressing the transitional costs requires well-designed government programs at the state and local levels. Curtailing international trade through tariffs is not a long-term remedy and does more total harm than good.

China as a disruptor

One valid complaint about the global economy’s balance is the outsized concentration of manufacturing output in China: China produces nearly a third of the world’s manufacturing output, despite producing less than a fifth of the world’s total output valued at market exchange rates. Not only does this configuration heighten security and supply-chain risks worldwide, but the speed and scope of China’s progress into high-end manufacturing together with recent sharp falls in its export prices are creating distress among competing producers around the world. The imbalance reflects many factors, but policies that distort natural market functioning and create deflationary forces are playing leading roles, aggravating international tensions.

Moreover, as disruptive as China’s export dominance is for richer countries, it is especially so for less prosperous ones. China’s size and its continued dominance even in low-skill manufactures leave less room for poorer countries to advance on the basis of growing their basic manufacturing exports.

The answer to this problem is coordinated international pressure on China’s leadership, not the war of all against all that the US abandonment of multilateral trade cooperation threatens to unleash.

The cost and benefits of policies to address trade imbalances and manufacturing decline can be debated in terms of economics. But the main sense in which Trump seeks to rebalance the international trade system is to make its operation more favorable to US interests at foreigners’ expense. Trump argues that the system has long been unfair to America; rebalancing in its direction is portrayed as simple justified redress. But as I argued above, the postwar international trade system benefited the United States as well as the world, and laying the problems that have accompanied America’s overall success at the feet of globalization merely deflects attention from the real policy failures.

The postwar system in theory and practice

The postwar international trade system launched at Bretton Woods in 1944 under US leadership aimed to achieve more balance, transparency, and sovereignty than previous monetary systems:

Balance, by providing balance-of-payments financing, the possibility of exchange rate adjustments, and development finance with the goals of promoting widespread growth and avoiding localized depressions.

Transparency, through rules around international adjustment and trade policy.

Sovereignty, by supporting domestic macroeconomic action and trade safeguards in pursuit of full employment.

The overarching vision, informed by international experience during the Great Depression, was that beggar-thy-neighbor policies are negative sum, whereas trade expansion, supported by macroeconomic stability as well as trade policy liberalization, is positive sum and conducive to world peace and democracy.

Systems evolve, however, sometimes undermined by their very achievements. The vibrant international trade and financial system being attacked today did not come on the scene all at once but emerged gradually over the postwar period through a process of initial success, transitional turmoil, and regeneration.

The Bretton Woods monetary arrangements were based on countries pegging their currencies to the US dollar, while the United States promised to redeem foreign official dollar reserve holdings in gold at a set price of $35 per ounce. This system gave America enormous power to dominate global monetary conditions, but also forced it to consider how its policies, including its support of global security, affected its ability to guarantee the gold value of global dollar reserves.

President Nixon ended the US gold commitment unilaterally in August 1971, thereby ushering in the end of the Bretton Woods fixed exchange rates. He believed that the system was unduly constraining US policy, inappropriately so as it had served its initial purpose of enabling recovery after World War II, including the emergence of Germany and Japan as major exporting powerhouses making inroads into American markets. In this sense, the success of Bretton Woods helped bring about its downfall.

At the same time, as Milton Friedman had predicted in the 1950s, the move to floating exchange rates had an important upside: It enhanced the policy freedom of the United States and the policy sovereignty of US trade partners, who now could deploy monetary policy in pursuit of domestic macroeconomic goals rather than dedicating it to fixing the exchange rate. For countries like Germany, importing inflation because of speculation that it would revalue its currency’s fixed dollar exchange rate, this was a relief.

Some predicted that floating exchange rates would cause fragmentation in international trade, and that the key international role of the dollar, which had been at the center of the Bretton Woods system, would weaken. The 1970s were indeed a turbulent decade in many respects, not the least of which was high inflation, but by the early 1980s, the global economy found a new policy equilibrium. Central banks learned how to use their monetary sovereignty to preserve price stability while steering the real economy. Validating another prediction of Friedman’s, the relief from balance-of-payments pressures that floating rates delivered allowed for further positive-sum liberalizations of international trade, as well as for growth in private international capital movements.

Finally, far from being finished as the premier global currency, the dollar solidified its reign, becoming effectively a global “currency among currencies” in international finance as well as trade. The pervasive role of the dollar in international invoicing and funding mitigated the potential negative effects of exchange-rate volatility on trade that skeptics of floating had voiced in the early 1970s. Global financial development helped too, by making hedging instruments available more widely and cheaply.

The last is one way that globalized financial markets have promoted trade and prosperity. In addition, they allow countries to share financial risks with each other and for the transfer of capital investments from countries where savings are abundant to countries where investment opportunities are attractive. Greater financial fluidity inherently allows for bigger and more persistent current account deficits and surpluses, but far from being a symptom of malign “imbalance,” these international credit flows are often a reflection of mutually advantageous and efficiency-enhancing trades.

That is not to say that financial markets never malfunction. To reduce those risks, a framework for international regulatory and supervisory cooperation emerged in the mid-1970s and has continued through bodies such as the Basel Committee on Banking Supervision, the Financial Stability Board, and the International Organization of Securities Commissions, the purpose of which is to plug cross-border gaps in prudential oversight and to avoid negative-sum races to the bottom in regulation. Nor are large current imbalances necessarily benign when they reflect potentially unstable financial processes (like the 2000s property price booms in the United States and some eurozone countries) or unwise macroeconomic policies (like the unsustainable US government budget deficit today).

After initial turbulence, the new international trade system that evolved after Bretton Woods produced unprecedented growth in global prosperity, certainly based on economic metrics but even more so when human development indicators such as infant mortality and longevity are considered. These benefits were not distributed evenly, either within or across countries, and some individuals and communities were net losers. Not everyone always played by the system’s rules. But globalization was much better for the world as a whole than the likely alternatives, and appropriate remedies for its failings were achievable based on international negotiation and domestic reforms.

Globalization reached its apogee amid the two decades of relative peace that followed the end of the Cold War. Not since the late nineteenth century had global commerce transited borders with so few geopolitical impediments. But in that setting, many governments lost sight of the need to base national security strategy on a firm base of social cohesion. As World Trade Organization head Ngozi Okonjo-Iweala accurately observed in a 2024 lecture, “Trade is sometimes blamed and scapegoated for poor outcomes that really derive from macroeconomic, technology, or social policy, for which trade is not responsible.”

Deforming international trade

Since January 2025, however, the world has entered an alternative reality, pushed by the United States. Higher US protection rates that vary across trade partners, especially if emulated abroad, will fragment international supply chains while raising costs for all businesses involved in international trade. The US shift from being a provider of global security to a source of global insecurity is prodding more countries to insulate their economies from disruption through measures that curtail trade or at least divert it from the United States.

The disruptions extend to finance. For one thing, higher costs of product trade themselves have been shown to lead to impaired financial integration among countries. Possible breakdowns in international regulatory cooperation could create incentives for governments to protect their financial markets, or if not, to join a regulatory race to the bottom that makes financial instability—another negative-sum outcome—more likely. Trump-aligned commentators like Lighthizer raise the possibility of financial inflow taxes, another form of tariff, as a way to reduce US external deficits, while expropriation fears in a troubled geopolitical environment may limit cross-border financial flows, as John Maynard Keynes predicted in a similarly turbulent environment in the 1920s.

A related disruption to international markets, in trade as well as finance, would be a more fragmented currency landscape in which the dollar’s status slips and other currencies like the euro and yuan gain ground. Several factors are joining to erode global confidence in the dollar, including Trump’s attacks on Fed independence, the US government’s unbridled issuance of dollar Treasury debt, the rising unreliability of US security commitments, the decline in US respect for the rule of law domestically and internationally, self-dealing by government officials, arbitrary US government interventions in private business, and the politicization of US official financial support (swap lines to Argentina, which desperately needed one, and a contemplated one to the United Arab Emirates, which has much less need). Dollar swap facilities have long supported the dollar’s use in offshore markets, and fears that the United States may weaponize them or other aspects of the global dollar network are spurring searches for insulation. Swaps may serve geopolitical goals of the United States, but selective and unconditional deployment to US “friends” could make other countries fear that US support of their dollar use will come with strings. A global economy without the dollar as a true universal standard of value and medium of exchange will be more uncertain and less efficient.

The Trumpian approach to economics promises more wasted resources as it abandons time-tested principles that have promoted prosperity and convergence in the past. It asks Americans to forgo the optimistic and outward-looking approach that promoted global democracy and peace over decades for one based on scapegoating foreigners. It is driven by a belief that there is a fixed global economic pie that must be redistributed in favor of Americans. This zero-sum view of economic policy, when implemented widely by the world’s governments, leads to a negative-sum collective outcome. The result is a world in which all, Americans included, are worse off.

The world economy healed itself after the disruptions of the 1970s and emerged stronger. It was helped along by the collapse of the Soviet bloc. Today’s geopolitical prospects are different. We may not be so lucky this time around.

Maurice Obstfeld is a senior fellow at the Peterson Institute for International Economics and Professor of Economics Emeritus at the University of California, Berkeley.